June 17, 2026

Nine Months In, Signify CEO Is Ready to Show His Hand

With strategy decisions looming, Signify prepares to reveal its next chapter

In January, CEO As Tempelman made a promise. On Tuesday, June 23, investors will find out what it means.

That's when Signify holds its Capital Markets Day in Eindhoven. Five months ago, the CEO signaled that a portfolio review was underway and that parts of the business could face divestiture or harvesting. The details were sparse. Management said clarity would arrive in June. Now June is here.

The question before us is how CEO As Tempelman provides clarity about where Signify intends to compete and, possibly more importantly, where it doesn't.

Capital Markets Day presentations often become the blueprint investors use to evaluate management for years. Targets announced next week will shape expectations for growth, profitability, capital allocation and portfolio decisions well beyond 2026.

Since arriving as CEO in September 2025, Tempelman has spent nine months listening, reviewing, and diagnosing. On June 23, those conclusions become public. What emerges may not be a series of blockbuster moves. But it will signal how the company intends to respond to the scale of the challenge it faces.

The Business Problem Is Real

Start with what Tempelman inherited: a structurally declining company facing simultaneous pressure on multiple fronts.

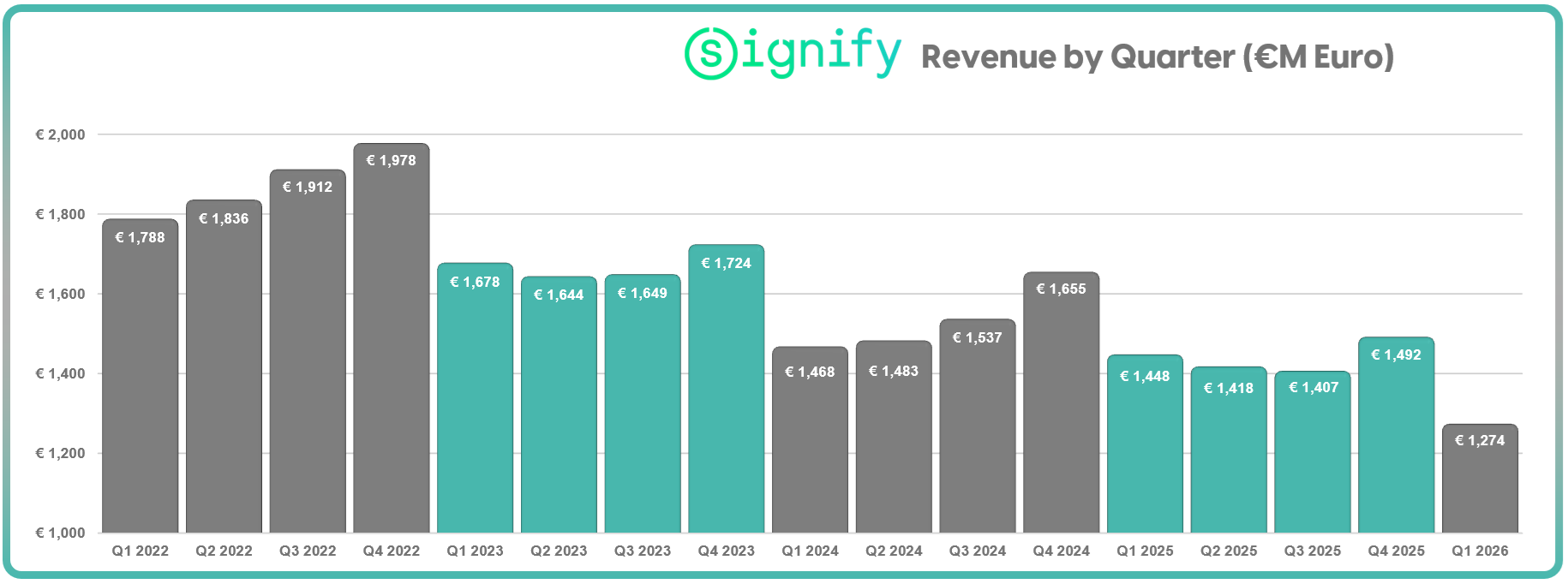

The revenue picture is unmistakable. Signify peaked in 2022 at €7.514 billion ($8.64 billion). By 2025, it had contracted to €5.765 billion ($6.63 billion). That's a 23 percent decline in three years. Recent quarters show the trend accelerating, not stabilizing.

Q1 2026 delivered €1.274 billion ($1.47 billion) in quarterly revenue, the lowest quarter since Signify's 2016 spinoff from Philips.

EBITA Margin by Business Unit

But the more revealing story is margin compression across every business unit. Professional is eroding. Consumer, the supposed growth engine, has experienced significant deterioration. OEM has almost become breakeven. Conventional is declining as designed, but it's doing so with high margins.

That's not one troubled division. It's a portfolio under simultaneous pressure. When Professional, Consumer, and OEM all compress at the same time, the problem isn't external. It's structural. Organizational complexity consuming returns. Fixed costs that don't flex as volumes decline. A company built to scale now trying to shrink.

This is what Tempelman was hired to address.

Nine Months of Diagnosis

His first move wasn't to announce restructuring. It was to understand the business from the ground up.

He visited markets. Talked to agents, specifiers, and system integrators. Reviewed the portfolio through multiple lenses: geography, segment, value chain positioning, growth potential versus harvest opportunity. By January 2026, that listening had produced results. Signify launched a strategic review and announced a €180 million ($207 million) cost program targeting 900 jobs.

By March, when he sat down with Inside Lighting at Light + Building, the strategic themes had crystallized and become consistent. Market-first thinking, not product-first. Portfolio review. "We can't be everything everywhere." North America as a top investment priority. The distinction between growth businesses and businesses designed to be harvested. Simplification rather than expansion.

Those weren't generic CEO observations. They were a roadmap. On June 23, investors see where that roadmap leads.

The Revenue and Margin Crisis Demands Portfolio Choices

Here's what the numbers are really saying: Signify can't invest everywhere. It doesn't have the cash generation or the management bandwidth to fix every business simultaneously.

Professional needs investment to stabilize. Consumer needs clarity on whether the retail channel is sustainable or whether the company should focus purely on connected systems and Hue. OEM is experiencing real cyclical pressure and requires a strategic decision: Is this a core vertical integration play with Advance drivers feeding Professional, or is it a cost center that no longer justifies its complexity?

2025 Sales by Business Unit

Conventional is designed to shrink. That's a managed process, not a crisis. But at some point, the economics of operating a declining legacy business in multiple geographies change.

And then there's the question of regional footprint. Signify operates 158 legal entities across 72 countries. Some of those are strategic. Others are legacy structures from past acquisitions. Some are likely small-scale operations whose strategic value deserves scrutiny.

The portfolio review is methodical because it has to be. These decisions will ripple through the company for years.

What the Agenda Reveals

The structure of Capital Markets Day offers clues about where Tempelman's thinking is headed.

CEO presentation. CFO presentation. Then three dedicated business deep dives: North America Professional (with Kraig Kasler, president of Cooper Lighting Solutions), Consumer, and India.

Kasler's appearance on the agenda is noteworthy. North America generates over one third of Signify's business, and North American executives don't typically take investors for a dedicated deep dive at Signify's Capital Markets Day. The move signals something worth parsing.

Tempelman has also emphasized that the U.S. market is a top investment priority. Consumer gets its own deep dive because, despite margin challenges, it remains brand-visible and defensible if properly repositioned around connected systems and Hue.

India's inclusion is the more interesting choice. It's not a top-five market for Signify. Yet it earned equal billing with the company's largest market and a core consumer brand. That suggests the narrative isn't about current scale. It's about manufacturing flexibility, long-term growth optionality, and the joint venture with Dixon Technologies that absorbed Signify's LED manufacturing footprint and is now targeting OEM business beyond Signify's own needs.

By contrast, OEM, Conventional, and regional structures get no dedicated agenda slot. That omission may send a message about what's under scrutiny.

The Cooper-Genlyte Question

Ever since the $1.4 billion acquisition of Cooper Lighting Solutions in 2020, lighting people have speculated about whether Signify would eventually consolidate Cooper Lighting and Genlyte Solutions in North America. Two organizations. Two agent networks. Many overlapping product categories.

Tempelman was asked directly about this during our March interview. His answer was measured: "My focus now is on making both companies the best they can be and very competitive." That's not the language of someone preparing a near-term integration announcement.

March 2026: Al Uszynski asks Signify CEO As Tempelman about Cooper Lighting Solutions and Genlyte Solutions business strategy in North America

Strategically, keeping things separate at this time makes sense. If Tempelman is orchestrating a global portfolio shift, destabilizing Signify's largest market with a major channel consolidation would be counterproductive timing. Better to stabilize the broader organization and complete the global transition before considering North American channel consolidation.

What's Actually Likely

Don't expect a series of blockbuster divestitures and announcements. In fact, smaller, targeted moves may carry more weight than big, headline-grabbing news. Expect disciplined portfolio decisions. Possibly:

- Continued harvesting of the $375 million conventional lamps business while maintaining profitability.

- Regional carve-outs where Signify operates in lower-priority geographies or through minimal structures.

- Manufacturing consolidation, possibly including closure or divestiture of smaller or redundant facilities.

- A clear assessment of OEM's role in the portfolio as both a vertical integration play supporting Professional and a B2B channel.

The company needs to answer a strategic question: Which parts of this portfolio belong together? Which serve a common purpose? Which would a focused competitor actually build from scratch?

That's not emergency restructuring. That's strategic portfolio management by a CEO who inherited a declining business and is making methodical choices about where to invest and where to optimize.

The Real Test

June 23 will be remembered not for what Signify announces but for whether Tempelman succeeds in communicating a coherent vision for a company that has become unnecessarily complex.

For years, Signify operated as a collection of businesses: Professional, Consumer, OEM, Conventional, plus Cooper, Genlyte, Hue, Wiz, Fluence, Color Kinetics, dozens of regional structures. The company competed in nearly every lighting category in nearly every global region.

That approach worked when markets were growing. It's untenable when revenues are declining and every business unit is under margin pressure.

The CEO faces a portfolio reality: declining revenues, compressing margins, fixed costs that don't flex, an organization stretched across many geographies and product lines. The question isn't whether changes are coming. The question is whether those changes are strategic and deliberate or reactive and fragmented.

Investors already know the problems. They want to see how management addresses the scale of the challenge.

Signify doesn't need to decide everything it wants to become. It needs to decide what it no longer wants to be.