July 16, 2026

Leaner Zumtobel Ends a Difficult Transition Year

Restructuring delivered savings while taxes and Components weighed on earnings

Zumtobel Group's annual report runs 244 pages. The story inside it is simpler than the tables and graphs suggest: the lighting business unit had a respectable year, and almost everything else conspired to bury that fact under a full-year profit figure that looks like a rounding error.

The Austrian lighting group closed fiscal 2025/26 on April 30 with revenue down 5.2% to €1.04 billion ($1.2 billion) and net profit reduced to just €1.0 million ($1.2 million), down from €15.5 million ($17.8 million) the year before. This year, shareholders will go without a dividend, a first in recent memory. The company's own press release calls this "cost discipline stabilizes profitability." That framing isn't wrong. It might just be incomplete.

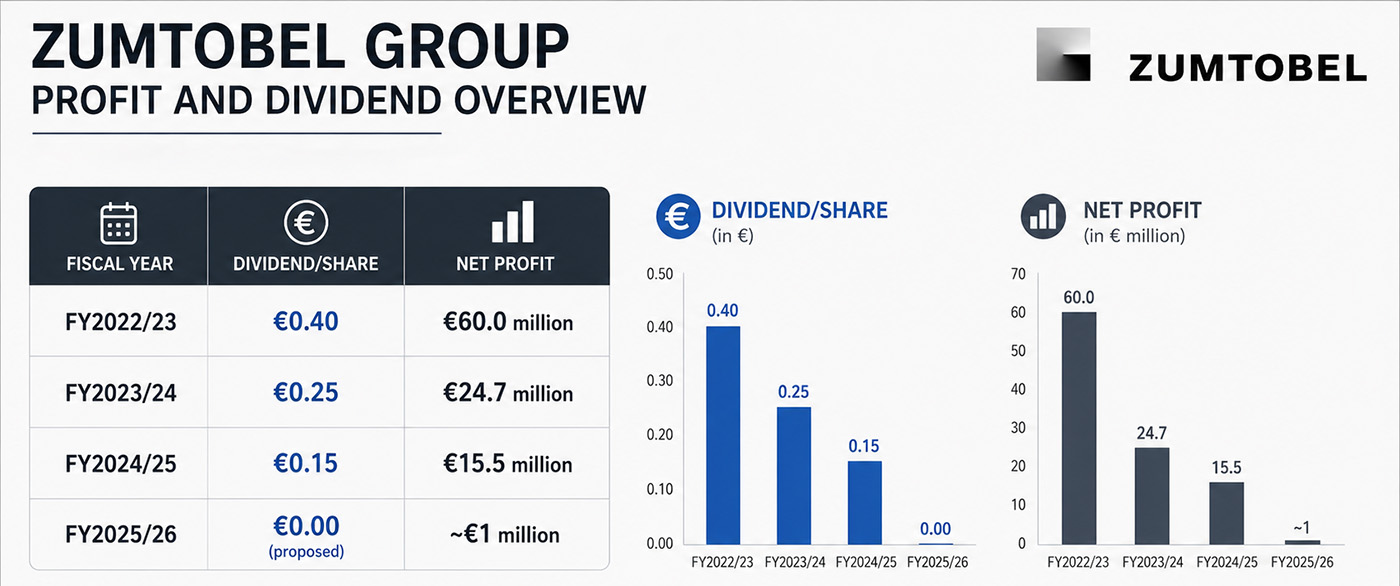

A Four Year Slide

This year's numbers don't arrive in isolation. Net profit has fallen every year since fiscal 2022/23, from €60.0 million to €24.7 million to €15.5 million to roughly €1 million now. The dividend has followed the same path, from €0.40 per share down to nothing. Zumtobel has been managing a shrinking earnings base for several years running, and this year is the point where the trend finally ran out of room.

Two Businesses, Two Different Years

Zumtobel operates through two main segments: Lighting, which covers the Zumtobel and Thorn luminaire brands, and Components, built around Tridonic, which makes the drivers and controls that go inside fixtures, including many made by Zumtobel's competitors.

Lighting had a decent year. Revenue slipped 3.7%, but the segment cut costs faster than sales fell, lifting adjusted operating profit from €51.3 million ($59.0 million) to €54.7 million ($62.9 million), a margin of 6.6%. That's not an impressive number against peers like Signify, Acuity or Legrand, but it's an improvement over last year's 5.9%.

Components did not have a solid year. The industrial sector that buys much of Tridonic's electronics stayed weak throughout, and the segment's adjusted profit dropped from €13.5 million to €4.6 million, roughly two thirds. Zumtobel also concluded that some of its past investment in Components product development would not pay off as expected, and wrote that value off entirely, along with the segment's remaining goodwill.

That struggle isn't unique to Dornbirn. At Signify's own Capital Markets Day last month, executives placed OEM and commodity manufacturing in a category of its own: still undecided, with continuing to run it in house, partnering it out, or divesting it all on the table. Two of Europe's largest lighting groups, within weeks of each other, are confronting the same open question. Manufacturing exposed to commodity pricing doesn't fit as neatly into either company's strategy as the branded fixture business does, and neither has settled on what to do about it.

Where the Profit Actually Went

Even with Components dragging on the numbers, Zumtobel still generated operating earnings for the year, roughly €10.7 million before tax. What finished the job was taxes. The company recorded an unusually large tax expense, €9.7 million, driven mainly by changes to how it accounts for expected future tax benefits in the United States, United Kingdom and Austria.

In plain terms, Zumtobel now expects to use fewer of the tax credits it has built up in those markets than it once assumed, and wrote down their value now. That single item did more to shrink the year's profit than anything happening on a factory floor.

That also means the American side of the business touched this year's results twice: once through the costs tied to shutting down U.S. production in Highland, New York, even as the company's U.S. leadership has maintained that manufacturing there continues, a divergence we've covered closely, and again through this tax adjustment.

A Leaner Company, For Now

The efficiency push behind the cost discipline language is real. Total headcount fell to 5,188 from 5,516 over the year, part of a broader restructuring program the company expects to keep paying off through the end of the decade.

None of this points to a company in crisis. It points to a company absorbing a difficult transition year in one part of the business while its core lighting operation holds its footing, at the tail end of a four year earnings slide that a strong tax bill made considerably worse.

For lighting people, the more useful test comes next year, when the tax noise clears and the industry finds out whether the slide has actually stopped.