June 24, 2026

7½ Signals from Signify's Capital Markets Day That Matter

Left to right: Signify Executives Sumit Joshi, Michael Kühne, As Tempelman, Željko Kosanović and Kraig Kasler.

Image credits: Signify Capital Markets Day

From Cooper's momentum to Genlyte's turnaround, the company sorted strengths from challenges

The last time Signify held a Capital Markets Day, Cooper Lighting people were still onboarding in the wake of a $1.4 billion acquisition that had closed just months before, supply chains were seizing up globally, and COVID was rewriting the rules of how buildings got built, occupied, and lit. Five and a half years later, the company that emerged from all of that arrived in Eindhoven on Tuesday with a CEO who inherited its worst revenue numbers since the 2016 spinoff from Philips and a public promise to explain what he intended to do about them.

CEO As Tempelman made that promise in January. On Tuesday, he delivered on much of it. Investors and analysts got six portfolio choices, three performance playbooks, and a set of 2029 financial targets. Other questions left the room unanswered.

Some of those may be the ones that matter most. Embedded in Tuesday's presentation were signals about North America, connected lighting, and the shape of the business Tempelman is trying to build that pointed well past 2029. The most consequential choices Signify faces may not appear in any earnings deck for at least a few quarters.

Inside Lighting was the only global trade media outlet granted an interview with CEO As Tempelman following the event, conducted as a 30-minute one-on-one Teams meeting. What he said during that conversation filled in some of what the presentation left open. Here are seven signals worth tracking.

Signal 1: The 0% to 1% Growth Target Should Be Read Carefully

Signify's official 2029 comparable sales growth target is 0% to 1%. Management framed it as a stabilization story: halting a multi-year revenue decline and returning to modest growth. The company's topline has contracted from €7.5 billion ($8.63 billion) in 2022 to €5.8 billion ($6.67 billion) in 2025, a 23% decline in three years. The 2026 guidance range of 7.5% to 8.5% adjusted EBITA margin sits below the 8.9% the company delivered last year, which means the expansion path to the 10% target runs entirely through 2027, 2028, and into the target year.

Read alongside that guidance, the 0% to 1% growth range carries a plausible alternative interpretation: the company may be building in the possibility that revenue continues to contract before the Build portfolio can generate enough momentum to offset continued Harvest decline. Getting to flat by 2029 may require recovering ground that has not yet been lost.

Above: Signify Chief Financial Officer, Željko Kosanović

Tempelman acknowledged the math honestly. "Lighting only offers so much growth opportunity," he said in our interview, "especially if you look at the time horizon, three, five years out." The Build portfolio is expected to grow at approximately 2% annually by 2029. The Harvest portfolio is projected to decline at roughly 5%. Those two curves have to cross at the right moment. There is little margin for a slow start.

Signal 2: The Company Is Already Scouting Life Beyond Lighting

That growth constraint is precisely why one of Tuesday's most consequential discussions had nothing to do with luminaires. Tempelman opened the door explicitly to adjacent markets, describing a framework for evaluating businesses where Signify has a genuine right to compete: a technical capability, a route-to-market, or a customer relationship that extends naturally into new territory. The examples he named included HVAC integration, smart-city infrastructure, building systems, and the operational data that connected lighting networks generate as a byproduct of doing their primary job.

Above: Signify CEO As Tempelman at Capital Markets Day, June 23, 2026. Image credit: Signify

In our interview, Tempelman described what that looks like in practice. In Europe, Signify already feeds occupancy data from connected lighting systems into HVAC controls. "You may say, "What is the occupancy of this room, and how do I set HVAC ahead of the temperature reading? Because temperature sensors are always behind the curve." Street lighting data, he added, is being used to operate traffic systems more intelligently. None of these adjacencies appear in the 2029 financial targets. They are being explored, not counted. What they become depends on whether the core business stabilizes fast enough to free up capital and management attention for what comes after lighting.

Tempelman told Inside Lighting that entry into a "next door" or "adjacent space" would likely occur “inorganically”, with acquisitions among the likely options if Signify identifies a business where it has a "right to play."

Signal 3: Cooper Lighting Is the North American Flagship

The event's agenda communicated something before a single slide appeared. After Tempelman's CEO presentation, three businesses received dedicated investor deep dives: Consumer, North America Professional, and India. Cooper Lighting Solutions occupied its own slot, with President Kraig Kasler presenting directly to investors. That kind of stage time, at a company Capital Markets Day, is not incidental. North American executives do not typically take investors for a dedicated deep dive at Signify's events.

Above: Cooper Lighting President, Kraig Kasler. Image credit: Signify

The presentation identified Cooper as holding the clear number-two position in the North American commercial lighting market, which Signify estimates at $10.5 billion in 2025 with low single-digit growth. Cooper's agent network, 125-plus agencies with average tenure exceeding 20 years, was described as a structural competitive advantage in a market where the top four manufacturers control more than 60% of sales. Cooper's connected lighting revenues, growing at 19% annually since 2010 and now representing roughly 35% of Cooper's total revenues, formed the core of Kasler's growth argument.

In our interview, Tempelman described what he took away from visiting agents personally before forming his North American strategy. "The agent model is a very strong one," he said. "They find the projects, they're good at closing success, and the entire customer experience through the specification and commissioning process is super customer-centric." That observation flows directly into Cooper's roadmap, which calls for deeper agent engagement, upskilling on connected systems, and deploying agentic AI tools across the customer journey.

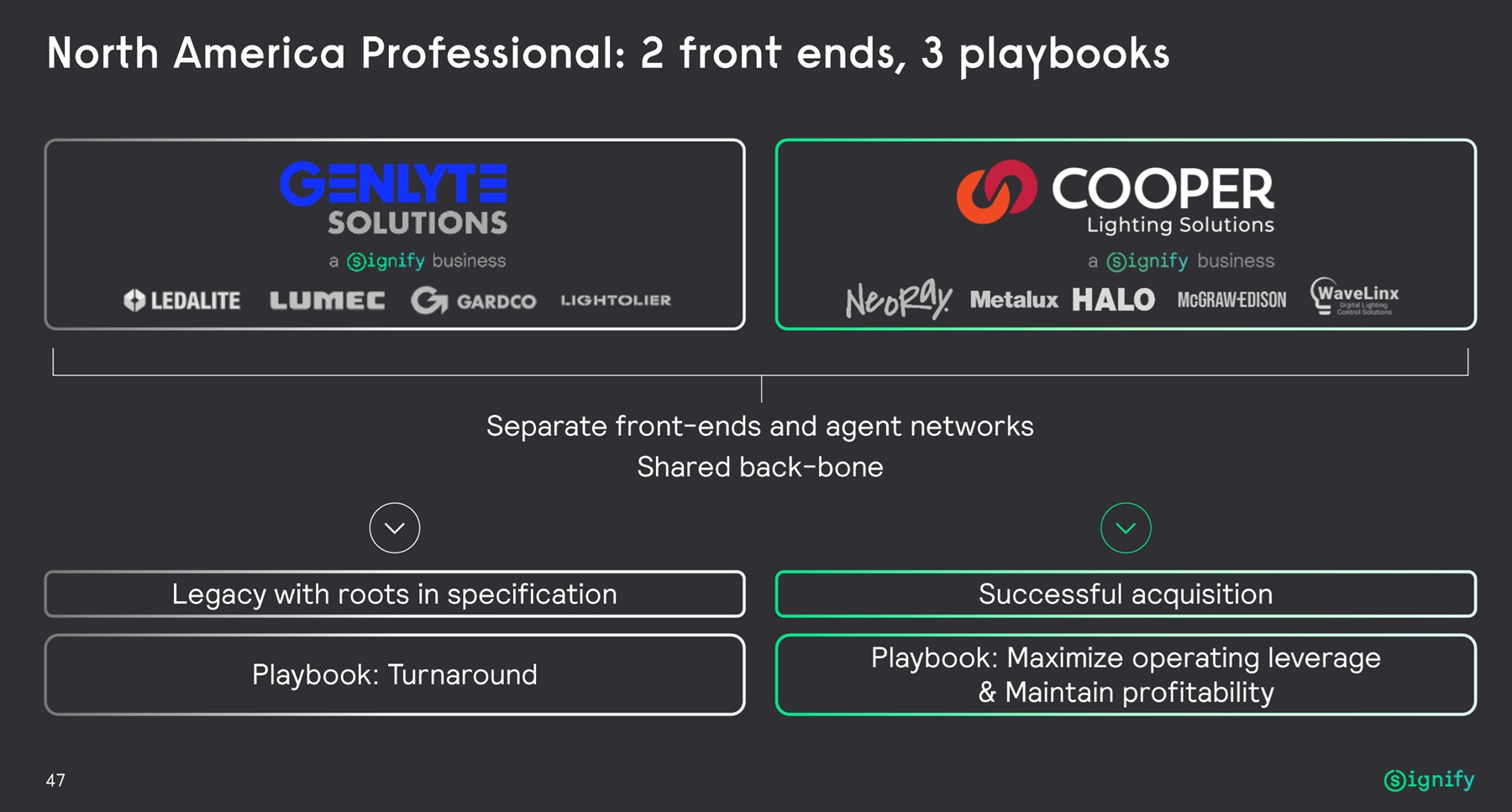

Signal 4: Genlyte Solutions Is on a “Turnaround Playbook”

The presentation formalized what the channel has known for some time. Cooper Lighting and Genlyte Solutions retain separate front-end structures and separate agent networks while sharing back-end infrastructure. The playbook assignments make the distinction explicit: Cooper runs Playbook 1, maximizing operating leverage and maintaining profitability. Genlyte runs Playbook 2. Turnaround.

That single word carries a specific meaning inside Signify. In Capital Markets Day language and in the CEO's own framing, Genlyte and the standard consumer LED lamp business are "EBITA dilutive." The phrase is corporate lingo for dragging the company's profits down. Genlyte is approximately one-third the size of Cooper, and the scale gap shapes both the urgency of the recovery and the resources available to fund it. Eighteen years after Philips paid $2.7 billion to acquire a company generating roughly $1.6 billion in revenue, Genlyte now occupies the turnaround slot inside Signify's North American portfolio.

In our interview, Tempelman offered the diagnosis without hedging. Genlyte has deep roots in specification and was historically strong through the conventional-to-LED conversion cycle. Over time it lost ground, particularly in stock-and-flow channels. "It's not as competitive in stock and flow as Cooper is," he said. The recovery path involves re-engaging agents, eliminating backend complexity, simplifying operations, and giving new leadership the clarity to rebuild channel relevance. Christy Tilton, recently promoted to Genlyte Solutions President, was described by Tempelman as having already "pieced that vision together."

What Genlyte stakeholders should take from Tuesday is straightforward: the company has committed to the turnaround publicly, on an investor stage, with a named playbook and named leadership. What remains to be determined is what success needs to look like before more changes are considered.

Signal 5: A.I. is Being Deployed as a Channel Tool, Not Back-Office Plumbing

Most lighting manufacturers currently discuss AI in the context of internal operations: inventory optimization, SKU rationalization, ERP integration. Signify presented AI as a customer-facing capability, and the Cooper roadmap put specifics behind that claim. Kasler described a future-state vision built around what the presentation called an "agentic AI layer that remembers, acts, and moves customers horizontally across the journey."

Today's tools handle discrete steps, augmented lighting simulation, a lighting and controls design platform, a configure-price-quote system, and AI-powered customer support chat. The roadmap connects those steps into a continuous experience: recommending products by project need, auto-building specs and submittals, creating bills of materials, and predicting delivery risks before they become jobsite problems.

Tempelman raised the same theme independently in our interview, applying it beyond Cooper to the broader channel strategy. "Whether that's around quotations, around pricing, around configurations," he said, "I think there are different parts of it that could be very suitable for AI applications."

Signal 6: The OEM Decision Is Still Unresolved, “All Options Open”

The phrase that appeared most often in both the presentation and Tempelman's on-stage remarks was "all options open." It applies to Conventional lighting and, more pointedly, to OEM and commoditized manufacturing. The presentation's Harvest choices included a specific line: reduce exposure to commoditized manufacturing, with all options open for OEM and commodity manufacturing operations. That phrasing, on an investor slide, is a signal worth taking seriously.

In our interview, Tempelman described three paths without committing to one: continue operating OEM because the vertical integration justifies its place in the portfolio, partner in some form, or divest. "Three options," he said, "and you've got to do the right thing here." He acknowledged the strategic value of having OEM inside the house: supply security, sourcing leverage, R&D proximity, the ability to innovate faster when the manufacturing and engineering teams share a building.

He also acknowledged that those benefits have to be weighed against the complexity costs. A divested or restructured manufacturing operation could mean different fulfillment partners, different lead-time profiles, and different inventory risk equations on stocking orders. It’s hard to imagine Advance LED drivers being outside the Signify portfolio, but the evaluation is active. The outcome is not yet determined.

Signal 7: Focus Beats Footprint

The world’s largest lighting company aims to make its world more focused.

The geographic consolidation from 55 to 35 active countries of direct presence is the most structurally significant decision in the entire portfolio framework. Those 20 departing countries are not being abandoned; they shift to distributor models or reduced operational footprints. The effect is that capital and management attention currently spread across markets that generate marginal returns get redirected toward the markets that generate real ones.

Signal 7½: A Blunt Question for Kraig Kasler

One of the more pointed moments of the investor Q&A came when an analyst from APG directed a question to Cooper Lighting President, Kraig Kasler. Referencing Tempelman's emphasis on benchmarking, he asked: "If I benchmark you against your peer, how far are you off from your benchmark?"

Kasler didn't flinch. He acknowledged a profitability gap with the market leader, attributed it to three factors: scale advantage held by the number-one player, a business mix that is still shifting toward specification and connected, and a head start the competition had on operational and supply chain improvements, accelerated by ownership continuity that Cooper lacked through the acquisition period and COVID years. "We think we have a long runway ahead there," he said, "and are already closing that gap."

The unnamed number-one player in North American professional lighting is Acuity, Inc. , whose trailing twelve-month Acuity Brands Lighting (ABL) revenue stands at approximately $3.6 billion. Cooper Lighting was a $1.7 billion business when Signify acquired it in 2020, and based on figures disclosed in Signify's 2025 annual report, it appears smaller today than at the time of acquisition.

Zooming out to total Signify North America, which encompasses Cooper alongside the Genlyte portfolio and lamps businesses, the combined footprint comes to roughly $2.7 billion, compared to ABL's $3.6 billion.

Why North America Might Matter More Than Ever

Over the past four months, we have sat down with Tempelman twice: at Light + Building in Frankfurt in March and virtually via Teams on Tuesday. In both conversations, North America has been named explicitly as a top investment priority.

The Capital Markets Day formalized what those interviews suggested. North American Professional revenues represent approximately half of Signify's total Professional segment, the company's largest business unit by revenue. The U.S. and Canada are emphatically among the 35 countries that get the focused version of Signify. The restructuring happening elsewhere is, in part, what funds continued investment here.

For lighting people working in this market, that is not a minor footnote to a global reorganization. The agents, distributors, specifiers, and contractors operating in North America are working inside a geography that Signify has staked its medium-term recovery on. The question is whether the execution, from Cooper's gap-closing roadmap to Genlyte's turnaround to connected lighting's growth targets, can validate the confidence the strategy places in this market.

By 2029, the answer will be visible in the numbers. For now, the bet has been placed.