June 10, 2026

What the Books Reveal About LSI's Largest Acquisition

Beneath the headline price, Royston’s numbers and disclosures tell more

When LSI Industries announced its $325 million acquisition of Royston Group in February, the headline numbers were clean and compelling: $272 million in trailing revenue, 14% EBITDA margins, a platform built for national retail rollouts. The story told itself.

And now, the audited financials have arrived.

Filed with the SEC on June 5, LSI's acquisition disclosure contains the kind of detail that press releases rarely volunteer. But before getting to the numbers, some context helps explain why this deal matters beyond its size.

A Company That Remade Itself Around Vertical Markets

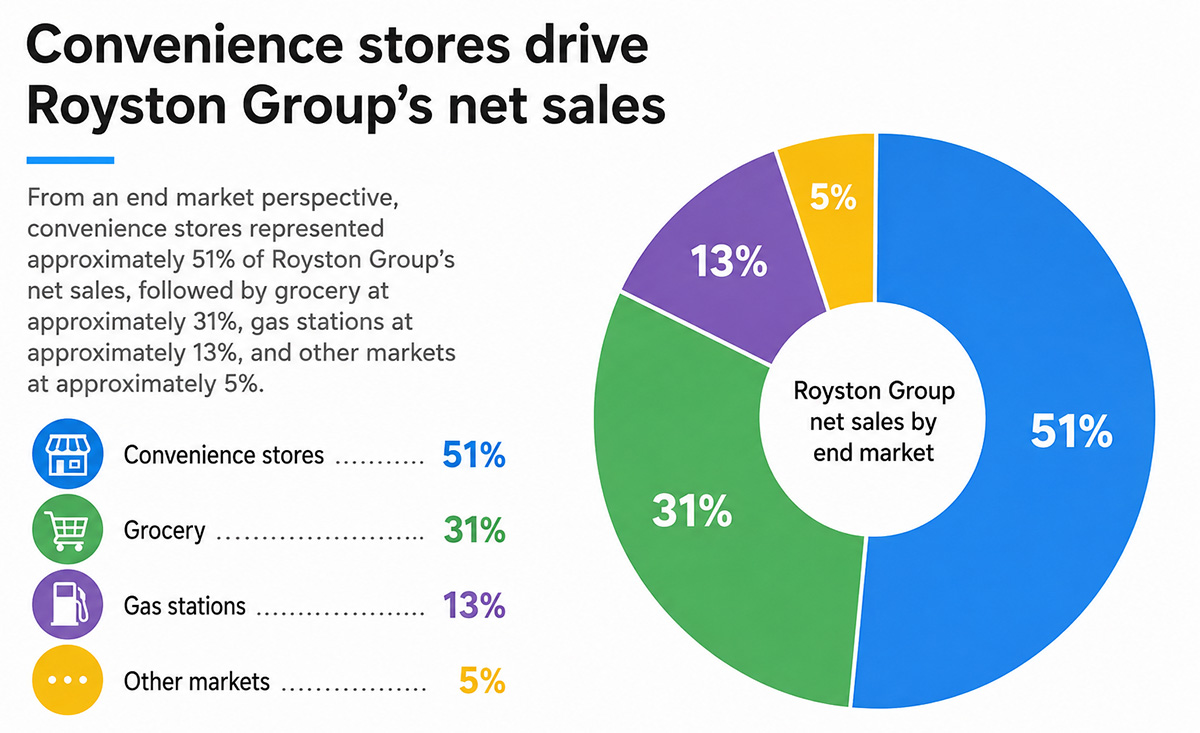

Five years ago, Lighting accounted for 62% of LSI's full-year revenue. By the first half of fiscal 2026, that had already reversed: Display Solutions led at 55.4%, with Lighting contributing 44.6%. Royston accelerates that shift dramatically. Pro forma combined revenue now exceeds $850 million, with more than 60% tied to convenience stores, gas stations, and grocery chains.

That concentration is deliberate. LSI has methodically built a portfolio oriented around national accounts operating thousands of locations, the kind of customers that run continuous remodel cycles rather than one-time construction projects. Once embedded with a chain at that scale, the business tends to stay. It is quieter than bid-driven commercial lighting work, and considerably stickier.

The acquisition history makes the strategy visible. Atlas Lighting Products ($97.5 million, 2017) was LSI's last major Lighting segment purchase. Everything since has fed the Display segment: JSI Store Fixtures ($90 million), EMI Industries ($50 million), Canada's Best Holdings ($24 million plus earnouts), and now Royston at $325 million-plus. LSI is not a lighting company that also does display work. At this point, the description runs the other direction.

1. Customer Concentration Is Significant

Royston's audited financials reveal that three customers accounted for roughly 44% of 2025 revenue. Customer A represented 20% of sales. A year earlier, that same customer represented 30% of revenue and 52% of receivables. The concentration has moderated, but it remains substantial.

This cuts directly against the stickiness narrative that makes Royston attractive. National chain accounts with multi-location remodel programs are exactly the recurring, relationship-driven business LSI is building around. The same dynamic that makes those accounts valuable makes losing one of them consequential. LSI inherits both the upside and the exposure.

Royston counts three of the largest five U.S. convenience store and grocery store chains among its customers, along with four of the largest five U.S. gas station chains. The company's own website features application photos from Wegmans and Circle K.

2. The Real Price Tag Is $338 Million

The $325 million headline figure was accurate as far as it went. The filing shows LSI pre-funded $13.2 million as an estimate of cash and working capital acquired, bringing total purchase consideration to $338.2 million. The company also absorbed $6.5 million in acquisition-related costs. Neither number was hidden, but neither appeared in the February announcement.

3. Revenue Was Declining Slightly Before the Deal Closed

The trailing twelve-month figure cited in February, approximately $272 million, was drawn from the period ending September 2025. The audited full-year financials show a different trajectory: Royston generated $271.3 million in 2024 and $265.0 million in 2025, a decline of roughly 2.3%.

The offset is real. Operating income improved from $17.7 million to $23.0 million over the same period, pointing to genuine margin expansion even as the top line softened. LSI was not buying a distressed business. But it was buying a business whose revenue was moving in the wrong direction, at a multiple based on figures that predated that slide.

4. The Financing Stack Is Now Fully Visible

LSI funded the transaction through four sources: a $150 million revolving credit facility, a $200 million five-year term loan, $98.1 million in net proceeds from a public stock offering completed February 26, and cash on hand. The equity raise, which we flagged as significant when LSI loaded its shelf last October, was a central piece of the capital structure. How quickly that debt load can be serviced will depend on how well the integrated business performs, and how secure those top three customer relationships remain.

LSI’s vertical market logic is sound, the platform is real, and the embedded position with major national chains is not easily replicated. But the audited books offer a more layered picture than the announcement suggested, and for anyone watching LSI's evolution from luminaire manufacturer to national retail platform, the details are worth the read.