June 25, 2026

Acuity's Lighting Business Cools as Overall Revenue Grows

Soft lighting demand persisted, but higher-margin Intelligent Spaces kept the company on a growth trajectory

Three quarters into fiscal 2026, Acuity's pattern is clear enough that it barely requires explanation anymore. Total sales rise. The Lighting segment softens a smidge. Intelligent Spaces grows. CEO Neil Ashe talks about where he is taking the company next. Repeat.

Wall Street, for one, is not complaining. Acuity shares jumped roughly 16 percent in early trading Thursday after the company beat analyst estimates on revenue, adjusted earnings per share, and adjusted EBITDA. The stock's move echoed Micron, which was also surging on its own results, a reminder that markets right now are rewarding any company that can credibly tell a technology growth story. Acuity, while not an A.I. chip stock, is one of those companies today.

What the fiscal third quarter ended May 31 added to the company's running narrative was texture. Lighting demand, which Ashe described as soft on the call, showed signs of firming in the back half of the quarter after a stretch from October through January that he called the weakest period. He attributed part of the drag to the April 2025 tariff spike that pulled orders forward into the prior fiscal year, and separately cited the federal government shutdown as a factor that slowed project conversion.

What The Lighting Numbers Show

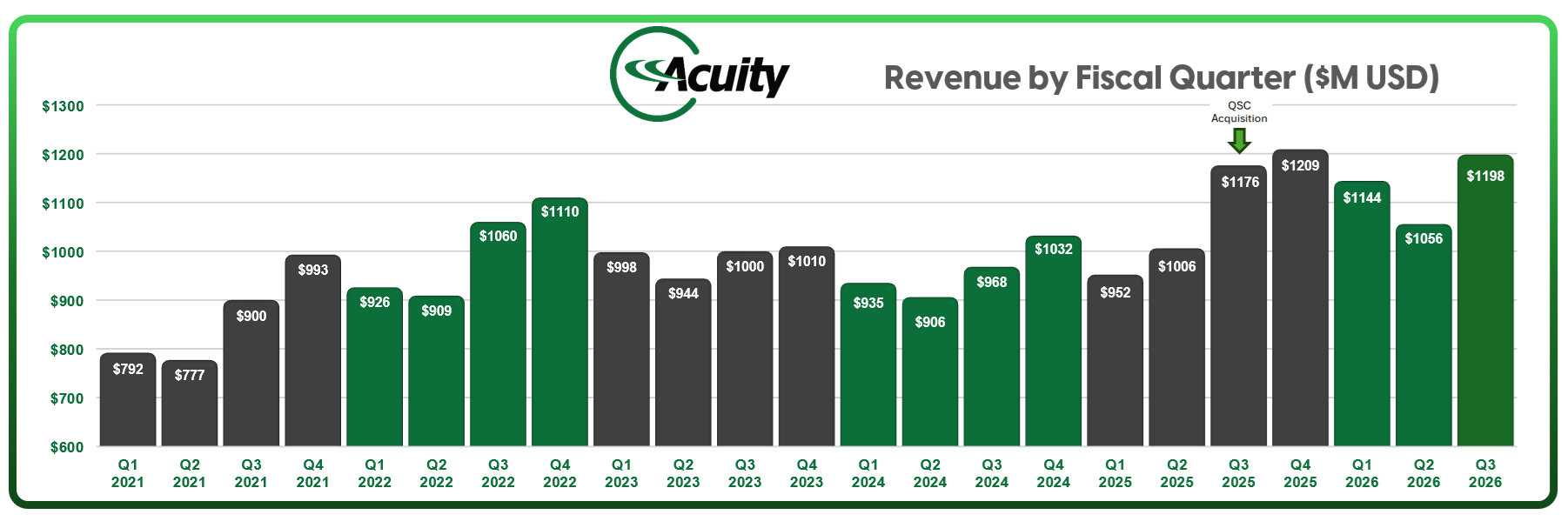

Lighting segment revenue came in at $905.2 million for the quarter, down 1.9% from the prior year, and is running down 1.2% through nine months at $2.62 billion. Within that, the channel breakdown is worth examining. The independent sales network, which accounts for the majority of how commercial lighting reaches the market, was essentially flat, up 0.8 percent in Q3. Corporate accounts grew 30% percent.

The direct sales channel fell 28% percent in the quarter and is down 23% percent through nine months, a decline that has now shown up in every quarter we have covered this fiscal year and deserves continued attention. This channel includes OEM sales, which has also been an underperforming segment for Signify over the last one to two years.

On margins, the segment held its position despite softer volume. GAAP gross margin ticked up 20 basis points to 46.8 percent, a result Ashe attributed to product discipline and supply chain improvements. When asked whether the Lighting segment can keep expanding margins even with revenue under pressure, Ashe answered simply: yes. On an adjusted basis, operating margin contracted 60 basis points to 18.2 percent, a more accurate reflection of where the segment actually stands.

The company also received a $6.4 million tariff refund during the quarter, which is excluded from adjusted results but benefits the GAAP figures.

Where Acuity Is Actually Growing

Intelligent Spaces generated $303.5 million in revenue for the quarter, up 14.9 percent, and now represents roughly 25 cents of every dollar Acuity takes in. Through nine months, the segment has produced $809 million in revenue. Its adjusted operating margin reached 25.1 percent in Q3, up 150 basis points, which is meaningfully higher than the Lighting segment's adjusted margin of 18.2 percent and reflects the software and controls character of the business.

Acuity's activity in the data center market was cited multiple times. Ashe confirmed that Distech's building controls platform is now actively targeting hyperscaler customers, and that lighting for data centers is growing as well, sold both directly and through prefab operators. He called it a "responsible entry" that should become a predictable portion of growth going forward. As a proof point, he cited Distech displacing an entrenched incumbent at Hartsfield Airport Terminal D, reportedly the first such displacement in more than 20 years at that facility.

Ashe also confirmed that Acuity is actively meeting with potential acquisition candidates on the Intelligent Spaces side, naming it among his top personal priorities for the quarter. He was clear that the standard is quality over volume, and held up the QSC acquisition as the model. For context, QSC remains a meaningful contributor to Intelligent Spaces revenue, though Ashe noted that data center growth at Distech specifically is entirely organic so far.

What Lighting People Should Watch

The direct sales channel decline is the number that most warrants ongoing attention from the lighting trade. A drop of 28% percent in a single quarter, following declines of similar magnitude in prior quarters, raises questions that the company has not yet answered in detail. Ashe has indicated no loss of market share in the Lighting segment overall, and the lighting agent sales network holding flat lends some support to that position. Agents comprise that's 58% of total company revenue, and 76% of Lighting segment revenue.

But the direct channel decline is large enough, and persistent enough, that it should stay on the radar.

Ashe also noted that the Architectural Billings Index (ABI), a widely watched forward indicator for commercial and institutional construction, has been negative for three years running, and said Acuity is not certain the index reflects actual activity on the ground. For a metric the industry often treats as a credible 9-to-12-month outlook, that is worth noting.

Ashe's stated first priority, repeated more than once on the call, is to build out Intelligent Spaces. That is not a criticism of the Lighting business, which is generating cash, holding margins, and showing early signs of demand improvement. It is simply where the company has chosen to invest its attention and capital. For agents, distributors, and specifiers whose business runs through Acuity's lighting brands, that distinction matters less in the near term than whether demand firming continues into the fall selling season.

That is the question the next quarter will begin to answer.