April 2, 2026

Acuity Posts Strong Quarter Amid Lighting Weakness

Earnings rise on margins and Intelligent Spaces growth despite soft core lighting demand

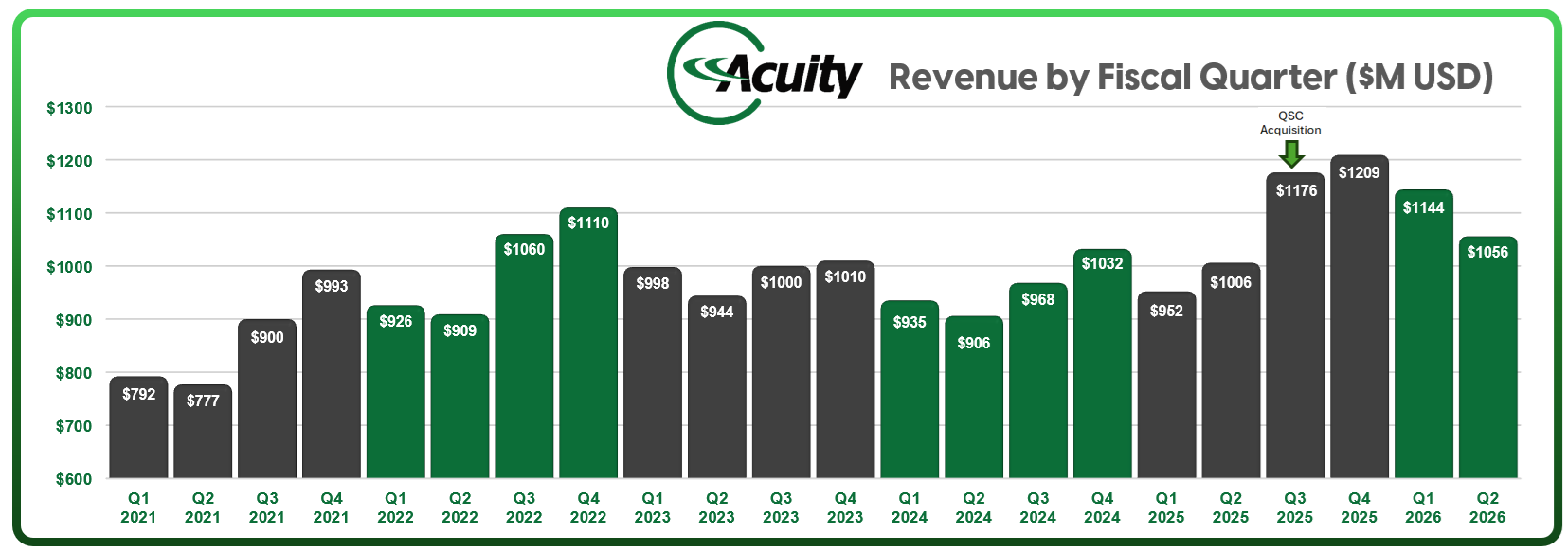

On its face, Acuity Inc.’s second quarter delivered much of what the market wanted to see: $1.1 billion in revenue, up nearly 5%, operating profit up 21%, and diluted earnings per share climbing 26%. Margins expanded. Cash flow was strong. The dividend went up.

It is the kind of quarter executives describe as “strong execution,” and CEO Neil Ashe did just that on the earnings call. But as we listen more closely — particularly to the tone and texture of that call — a more layered story emerges. Lighting People know this pattern well: when everything looks clean, it is often because something else is doing the heavy lifting.

That “something else” is not the lighting segment.

Acuity's earnings per share of of $4.14 beat estimates, while sales of $1.06 billion missed expectations. Acuity shares are off about 3% in early Thursday trading, more than doubling the broader market's loss, as the S&P 500 and Nasdaq each fall 1–1.5% in the wake of a presidential address Wednesday night on the U.S.-Iran war that signaled no clear end in sight.

The Lighting Segment: "Demand Delayed", Not Gone

The lighting segment declined 2.8% in revenue and saw operating profit fall 4% year over year. On the call, Ashe did not dispute the softness. Instead, he reframed it.

He pointed to two forces shaping demand. First, macro uncertainty. Customers are waiting for clearer direction on tariffs and interest rates before committing to projects. Second, and more unexpectedly, the rise of data centers. According to Ashe, data center construction is creating a “crowding out” effect, pulling labor and key inputs away from traditional commercial projects.

The result is not a collapse in demand but a slowdown in timing. Projects are sitting in the pipeline longer. “Conversion rates are about the same,” Ashe noted, but the time to release is increasing.

$ in millions | Three months ended

For the lighting agent sales network, that nuance matters. Agents, Ashe said, are still in hiring mode, signaling confidence that conditions will improve. But for now, the market feels stalled rather than shrinking. Lighting agents contributed 75% to Acuity’s lighting revenue in the quarter – a modest 0.2% improvement compared to Q2 2025.

While the Intelligent Spaces revenue surge of 44.7% is the quarter's headline-grabber, the "organic" nature of that growth requires a closer look at the calendar. This most recent quarter (ended Feb 28, 2026) includes a full three months of QSC results. By comparison, the prior-year period included only two months of QSC, which closed on Jan 1, 2025.

What did show up more sharply — though without much discussion — is the direct sales channel. Direct sales declined 27.5% in the quarter and 21.3% for the first half, attributed to “project business that did not recur.”

That explanation may be accurate, but it leaves open important questions. What specific projects drove prior-period strength? Were they one-time in nature, or indicative of share that has since shifted? A drop of this magnitude in a single channel is difficult to fully dismiss as timing alone, and it bears watching for signs of whether this is volatility — or something more structural.

Notably, Ashe pushed back on any suggestion of competitive erosion. “No indication that we are down in market share,” he said. Pricing, he emphasized, is deliberate and situational: “We price products related to the value they provide… no universal pricing strategy.”

Tariffs: From Headwind to Potential Upside

Even tariffs — typically a pressure point — were framed as manageable. Ashe described Acuity’s supply chain as “the most dynamic, well-executed in the industry,” a statement that reads as both reassurance and quiet assertion of competitive advantage.

What went unmentioned on the call — but disclosed in the 10-Q — is a more nuanced tariff backdrop. Following a February 2026 U.S. Supreme Court ruling on IEEPA tariff authority and a subsequent Court of International Trade decision, importers may be entitled to refunds on certain tariffs already paid. Acuity states that it has paid such tariffs, but that the outcome remains uncertain and no amount is disclosed.

That introduces a potential financial contingency with asymmetric upside: a recovery of previously paid costs that are not currently reflected in results. It is not yet actionable — but it is also not trivial.

Looking ahead, the outlook is cautious. The lighting segment is expected to be flat to down low single digits for the full fiscal year ending August 31. That is not a collapse. But it is not growth.

Margins Up, Volume Down — And Headcounts Reduced

Perhaps the most telling detail in the quarter is not the revenue decline but what happened alongside it: margins improved.

That dynamic — higher margins on lower volume — does not happen by accident. It is engineered. Strategic pricing, product mix, and productivity gains all contributed. But so did labor actions.

Acuity recorded approximately $6 million in charges tied to workforce reductions, primarily in factory operations. Ashe framed these as targeted moves to align cost structure with current demand. On a company of roughly 13,800 employees at the end of fiscal 2025, the scale is modest.

And that is precisely the point.

In a year when Signify announced headcount restructuring actions exceeding $200 million globally, Acuity’s approach looks surgical by comparison. This is not a sweeping reset. It is a calibration — focused on factory labor, not corporate headlines.

For the industry, the signal is subtle but important. Lighting demand is soft enough to require adjustment, but not broken enough to justify a full-scale restructuring.

Intelligent Spaces: Growth, Margins, and the Future

If the lighting segment is stabilizing, the Intelligent Spaces segment is accelerating.

Revenue surged more than $76 million year over year in the quarter, with operating profit and margins expanding sharply. For the first half, segment revenue more than doubled — up 106% — but that figure carries an important asterisk: QSC did not close until January 1, 2025, meaning the prior-year comparison reflects just one month of QSC results. Starting in Q3, those comparisons normalize and the headline growth rate will compress. The underlying business is genuinely strong. But the trajectory looks different once the acquisition math levels out.

The integration of QSC continues to pay dividends, and management made clear that future acquisitions will follow this path. Ashe noted that the company’s acquisition pipeline is now focused squarely on Intelligent Spaces.

This is not diversification for its own sake. It is a redefinition of the business.

The Intelligent Spaces segment sits at the intersection of controls, building automation, and audiovisual platforms. It is where software, data, and infrastructure converge. And increasingly, it is where growth lives.

Even discussions around artificial intelligence reflected this orientation. Ashe described the company as “AI maximalists,” suggesting a belief that AI-driven capabilities will enhance building performance and user experience. The nuance, he hinted, is that while many will claim AI benefits, the real advantage will come from integrating data across systems — something this segment is designed to do.

Capital Allocation, Memory, and a Subtle Rebalance

The financial backdrop reinforces the strategic shift. Acuity generated nearly $230 million in operating cash flow in the first half and returned significant capital through dividends and buybacks. Debt tied to the QSC acquisition continues to come down.

At the same time, Ashe acknowledged supply chain dynamics tied to memory markets — an issue more relevant to the Intelligent Spaces segment than traditional lighting. It is a reminder that as the company leans into technology, it inherits a different set of dependencies and risks.