March 24, 2026

Energy Focus Down to 8 Full-Time Employees, $3.6M in Sales

Leadership once again warns about its ability to continue as a going concern

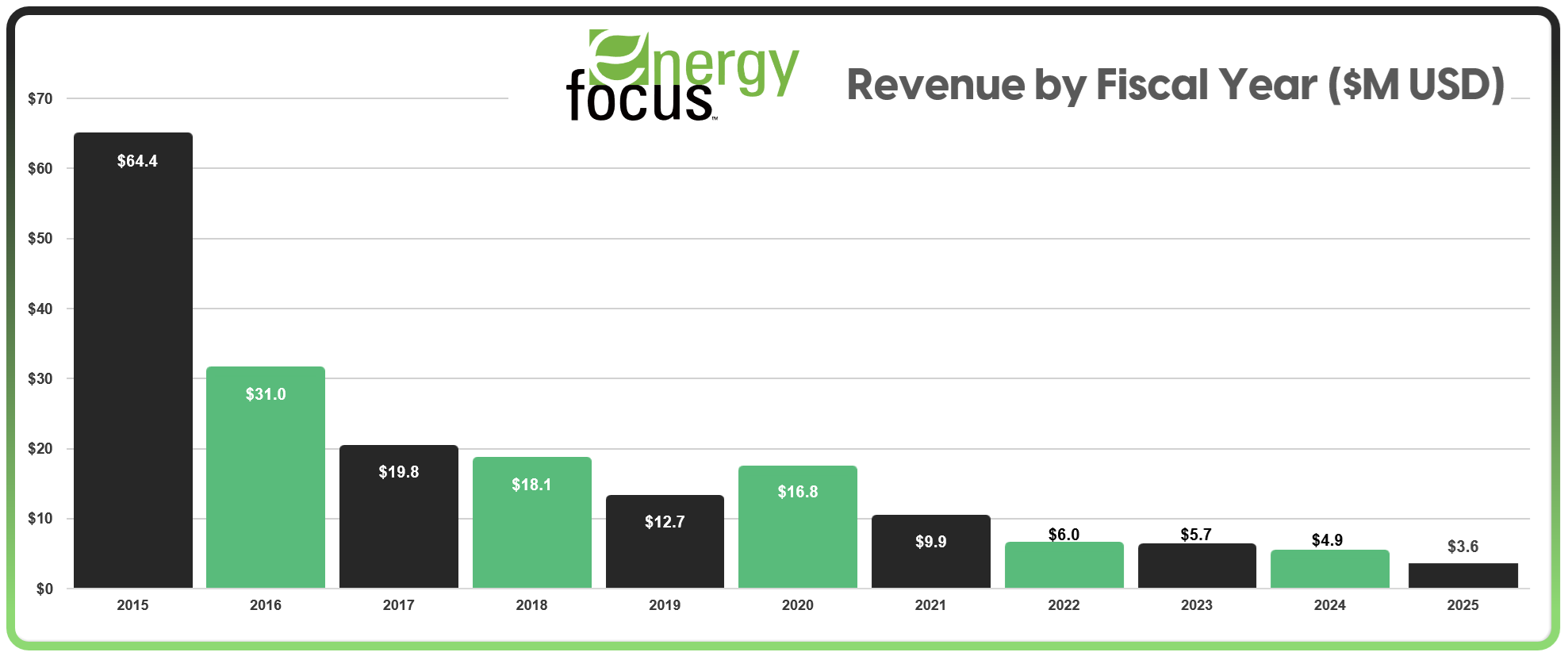

In 2015, publicly traded Energy Focus reported $64.4 million in annual revenue. Ten years later, it is a company of roughly eight full-time employees, generating $3.6 million and openly questioning its own survival .

That contrast frames everything in its newly released 2025 results, disclosed through a March filing that reads less like a routine earnings update and more like a company taking inventory of its remaining options .

Ohio-based Energy Focus still operates as a niche LED lighting manufacturer, serving commercial retrofits and military maritime applications. But its core is under strain. Revenue fell 26.7% in 2025, driven by a 42.7% drop in military sales, historically its most dependable segment .

The explanation is familiar: delayed federal budgets, uneven procurement cycles, and a market that no longer guarantees repeatable demand. Commercial sales improved modestly, but leaned heavily on a single $0.5 million UPS project in Taiwan. One deal, carrying outsized weight.

Customer concentration compounds the risk. Three customers account for 48% of revenue. In a business this small, that is not concentration. It is exposure.

For Lighting People watching from the sidelines, the pattern is less about one bad year and more about a system that no longer scales.

The Arithmetic of Survival

The company lost $1.0 million in 2025, bringing its accumulated deficit to $155.9 million. Losses have narrowed, but they have not disappeared.

Cash stands at approximately $1.1 million. That figure, on its own, is thin. The context matters more. The increase came largely from issuing stock, not from operations .

Throughout 2025, Energy Focus raised capital in increments. $200,000. Another $200,000. $500,000. Then $1.2 million. A pattern of small, continuous infusions that function less as strategic financing and more as ongoing support.

This is the company’s operating model, for now. Generate what revenue it can. Cut costs where possible. Fill the remaining gap with equity. Accept dilution as the price of time.

The Line That Changes the Tone

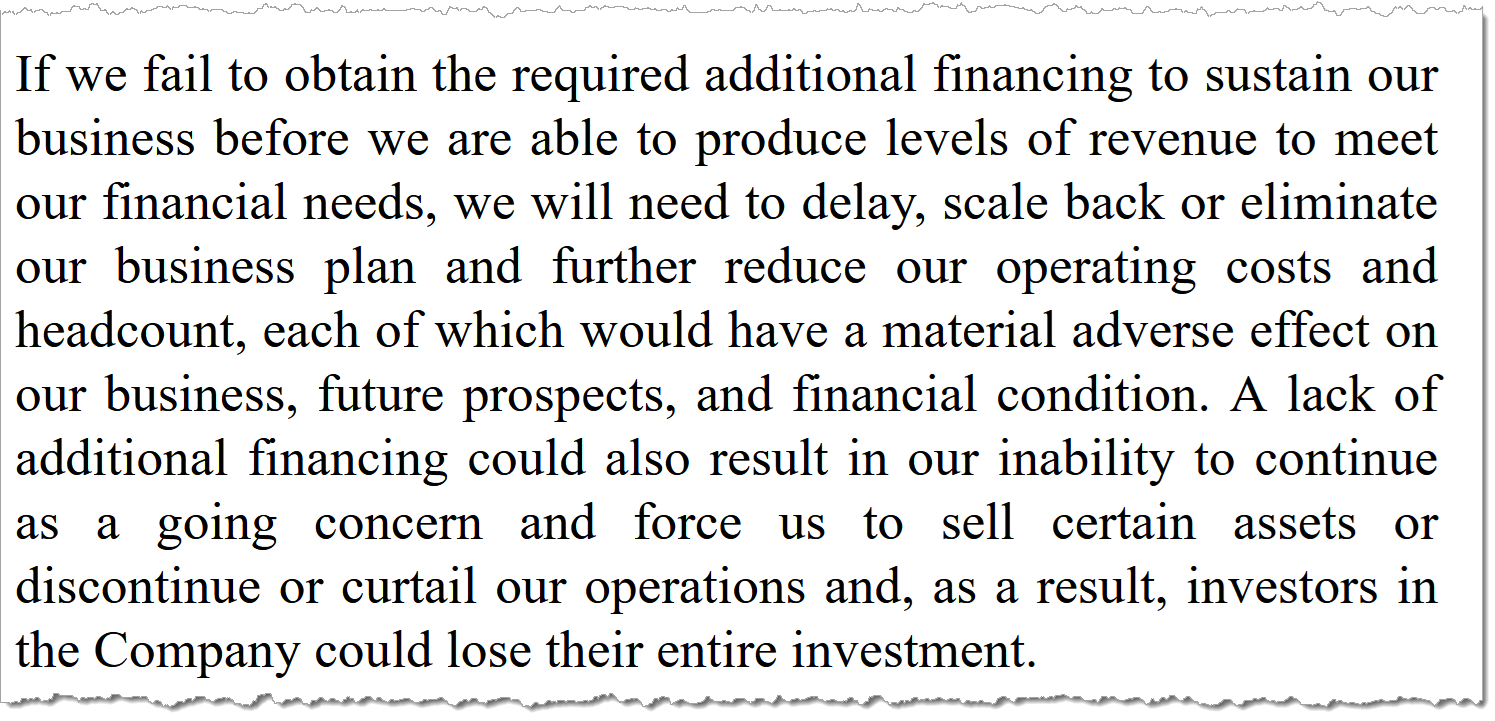

Buried in the filing is the sentence that reframes everything: substantial doubt about the company’s ability to continue as a going concern .

It is a technical phrase with plain implications. Without additional funding, the company may not sustain operations. Management acknowledges as much, outlining scenarios that include reducing headcount or curtailing the business entirely.

For a company already operating with a single-digit workforce, those are not distant hypotheticals.

The Pivot, and the Gap

Energy Focus is not standing still. It is attempting to reposition itself around energy storage, AI data center UPS systems, and advanced power technologies.

There are early signals. The Taiwan UPS project is one. Initial engagement with defense contractors is another. Expansion into Asia is framed as a path to new demand.

But these are early-stage efforts, entering markets that require capital, scale, and patience. Energy Focus has limited reserves of all three.

The strategy aligns with broader industry momentum. The constraint is execution.

Between Continuation and Conclusion

Energy Focus is no longer defined by what it was. Nor is it yet defined by what it hopes to become. It is a company in between. Shrinking core business. Persistent losses. A narrow cash position. A strategy that depends on markets it has yet to penetrate.

There is still a path forward. But it runs through capital markets, not operating cash flow.

For now, the company remains in motion. Still shipping. Still raising funds. Still pursuing relevance. But survival is no longer assumed. It is being recalculated, one quarter at a time.