April 24, 2026

Signify Sales Slide Again As June Decisions Loom

At Signify, everything is being managed, but not much is improving

Signify didn’t fix the business in the first quarter of 2026. It managed it at a level the company hasn’t seen before.

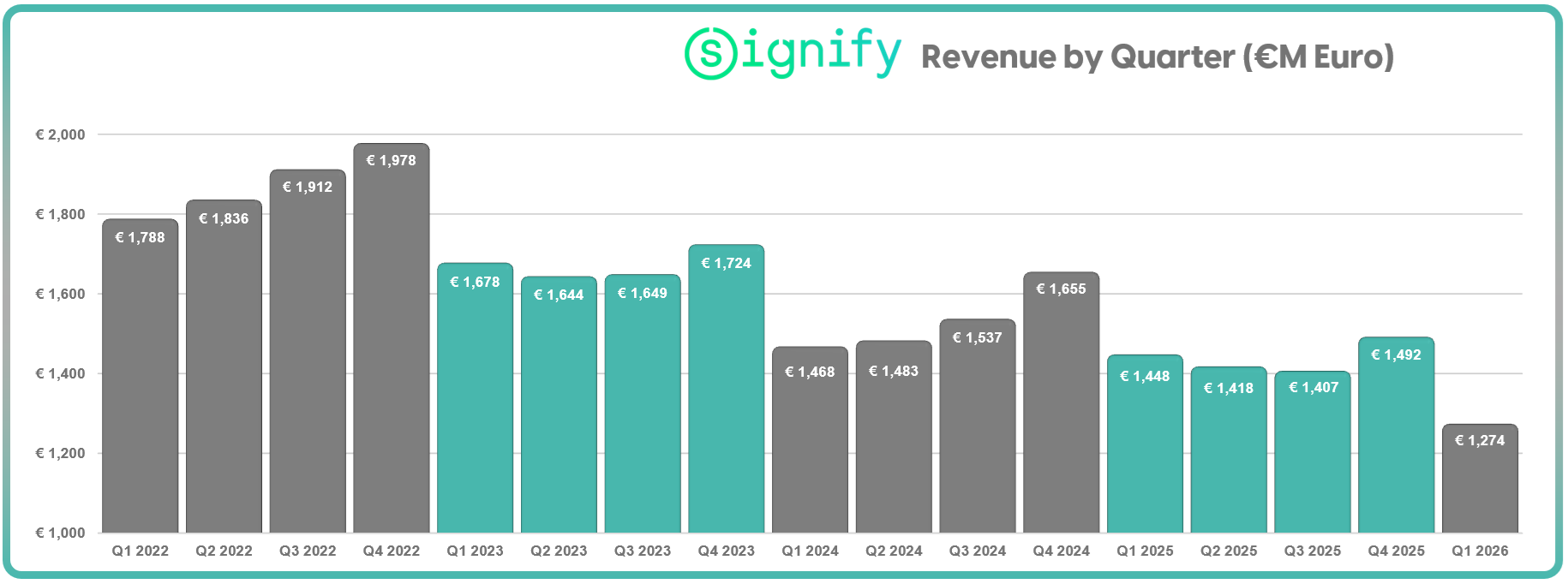

Revenue came in at €1.27 billion, down 12% year over year and, more notably, marking the lowest quarterly revenue since Signify spun off from Philips in 2016. That’s not an isolated dip. Four of the last five quarters have now set new lows, a pattern that persists despite years of acquisitions, including the 2020 addition of Cooper Lighting.

This is the kind of detail that doesn’t show up in a press release. But it reframes the quarter. The issue isn’t just that sales are down—it’s that the baseline itself has been resetting lower, repeatedly.

And yet, the company emphasized something else entirely: resilient margins, disciplined execution, stable cash flow. It’s a narrative of control in a business still searching for traction.

CEO As Tempelman, now in his first full fiscal year in the role, is managing through a set of global challenges he inherited. His tone is measured, even uplifting at times. But for lighting people watching closely, the more important question isn’t what improved this quarter. It’s what might be about to change.

At its upcoming Capital Markets Day, Signify is expected to do more than update investors. The company has already signaled that a portfolio review is underway, with potential divestitures, carve-outs, or “harvesting” decisions on the table. That makes Q1 feel less like a standalone performance and more like a bridge—one that carries the company toward a structural reset that hasn’t yet been fully revealed.

March 2026: (3:10) Al Uszynski asks Signify CEO As Tempelman about key strategy decisions ahead of Signify’s June 23 Capital Markets Day

Margins Holding Under Pressure

The headline numbers suggest stability. Gross margin held at 40.6%, a level many manufacturers would gladly defend in a down market. Free cash flow improved modestly year over year.

The underlying dynamics tell a more constrained story. Adjusted EBITA margin declined to 6.5% from 8.0%, reflecting lower volumes and the familiar challenge of fixed cost absorption. Net income fell sharply to €8 million, pulled down in part by €63 million in restructuring charges tied to a broader €180 million cost program.

On the earnings call, Tempelman framed the approach plainly: focus on what can be controlled, especially pricing and costs. That discipline is visible. So is the absence of demand-driven momentum.

A Soft Market, And Something More

Every major segment declined.

Professional was down 3.7%. Consumer dropped 4.6%. OEM fell 4.8%. Even allowing for currency impacts, the weakness cuts across the portfolio.

Management points to macro forces: tariffs, geopolitical instability, softer construction cycles, and persistent overcapacity. Those pressures are real, but they are not unique to Signify.

Peers offer a useful reference point. Acuity Brands’ lighting segment declined 2.8%. Zumtobel’s lighting division fell 5.1%. LSI Industries reported growth of 2%. Against that backdrop, Signify’s sharper top-line contraction raises more structural questions—particularly given its exposure to legacy businesses like conventional lamps, which declined 17.9% in the quarter.

This is a company navigating both cyclical softness and portfolio complexity at the same time.

A More Nuanced View From the U.S.

In the United States, the performance splits along product lines rather than geography.

"We've got two businesses in the US, the Cooper business and Genlyte Lighting Solutions. And Genlyte is particularly exposed to outdoor projects...we saw big weakness, while Cooper was more or less flat versus same quarter last year."

"So, I think Cooper has outperformed on the bigger portfolio in the indoor side; while Genlyte was more exposed to the outdoor side... we saw a drop."

— As Tempelman, CEO , Signify

Indoor lighting sector activity tied to Cooper Lighting has held up. Outdoor and public-sector exposure through Genlyte has not, reflecting delayed municipal spending or private project volatility. A recent leadership change at Genlyte Solutions highlights that this is an area under scrutiny.

The takeaway is less about regional strength and more about how different slices of the portfolio respond to the same environment.

Where the Story Gets More Complicated

As the quarter unfolds beyond the headline numbers, the narrative becomes more fragmented. Some areas are holding, others are stabilizing, and a few are simply lagging behind the broader market signals.

To make sense of it, it helps to break the business into its moving parts.

Consumer: Demand Holding, Signals Shifting

- Retail sell-out remains relatively strong, even as sell-in is pressured by inventory corrections

- Management acknowledged weakening consumer sentiment, but said it has not yet appeared in demand

- April trends suggest sell-in and sell-out are beginning to realign

The gap between sentiment and reported demand stands out. When confidence indicators decline while sell-through remains steady, it often reflects a lag rather than insulation. Channels may still be working through inventory, delaying the full effect.

OEM: Stabilizing, With Limits

- Comparable sales declined 4.8%, though less sharply than prior periods

- Pricing pressure has eased, improving margin dynamics

- No clear confirmation of volume recovery or demand acceleration

The language around OEM has shifted toward stabilization. What’s less clear is how much of that is driven by underlying demand versus pricing dynamics and easier comparisons.

Cost Actions: Carrying the Load

- €63 million in restructuring costs recorded in Q1 as part of a €180 million program to reduce 900 jobs – announced in January

- Headcount reduced to 26,008 employees, down 621 from the start of the year

- Headcount reductions remain in progress, with some delays tied to regulatory processes

Cost reduction is doing much of the operational work this quarter. The scale of headcount decline reflects both planned restructuring and ongoing volume adjustments. Execution, however, is still incomplete.

Inflation: Pressure Still Building

- Management flagged exposure to energy, plastics, and commodity costs

- Regional impacts vary, with markets like India experiencing sharper increases

- Pricing actions are being deployed selectively across products and geographies

Notably, much of this pressure is forward-looking. The first quarter reflects only part of the cost environment the company expects to navigate through the year.

Guidance and What’s Missing

- Adjusted EBITA margin guidance maintained at 7.5% to 8.5%

- Free cash flow outlook held at 6.5% to 7.5% of sales

- No full-year revenue guidance provided

The absence of a revenue outlook stands out. Officially, it reflects uncertainty. Practically, it may also reflect business units and product portfolios that are still being reshaped.

June 23: The Next Moment That Really Matters

The Capital Markets Day has been positioned as the point where strategy becomes explicit.

Management has indicated that the portfolio review will address where the company intends to invest, where it will optimize, and where it may step back. That includes the possibility of divestitures or structural changes across parts of the business.

For a company with a footprint as broad as Signify’s, those decisions are unlikely to be simple or singular. More likely, they will unfold across regions, product lines, and legacy structures that have accumulated over time.

A Company Still Defining Its Direction

There is a steadiness to Signify’s execution right now. Tempelman is managing costs, preserving margins, and maintaining operational discipline in a difficult environment. That matters.

What remains less visible is the path to renewed growth.

The first quarter shows a company in transition—one that is controlling what it can while preparing for decisions that could reshape what comes next. For now, the business is being managed carefully. The broader direction is still taking shape.

June 23 should bring that into sharper focus.