June 23, 2026

Dialight Doubles Profit, Revenue Nears Decade Low

After years of restructuring, profits are back. The $70 million in lost annual revenue is not.

Dialight's fiscal year 2026 results contain two companies inside one report: an industrial lighting manufacturer that has gotten remarkably good at running itself, and one that keeps selling less product. Understanding which version wins from here is the only question that matters.

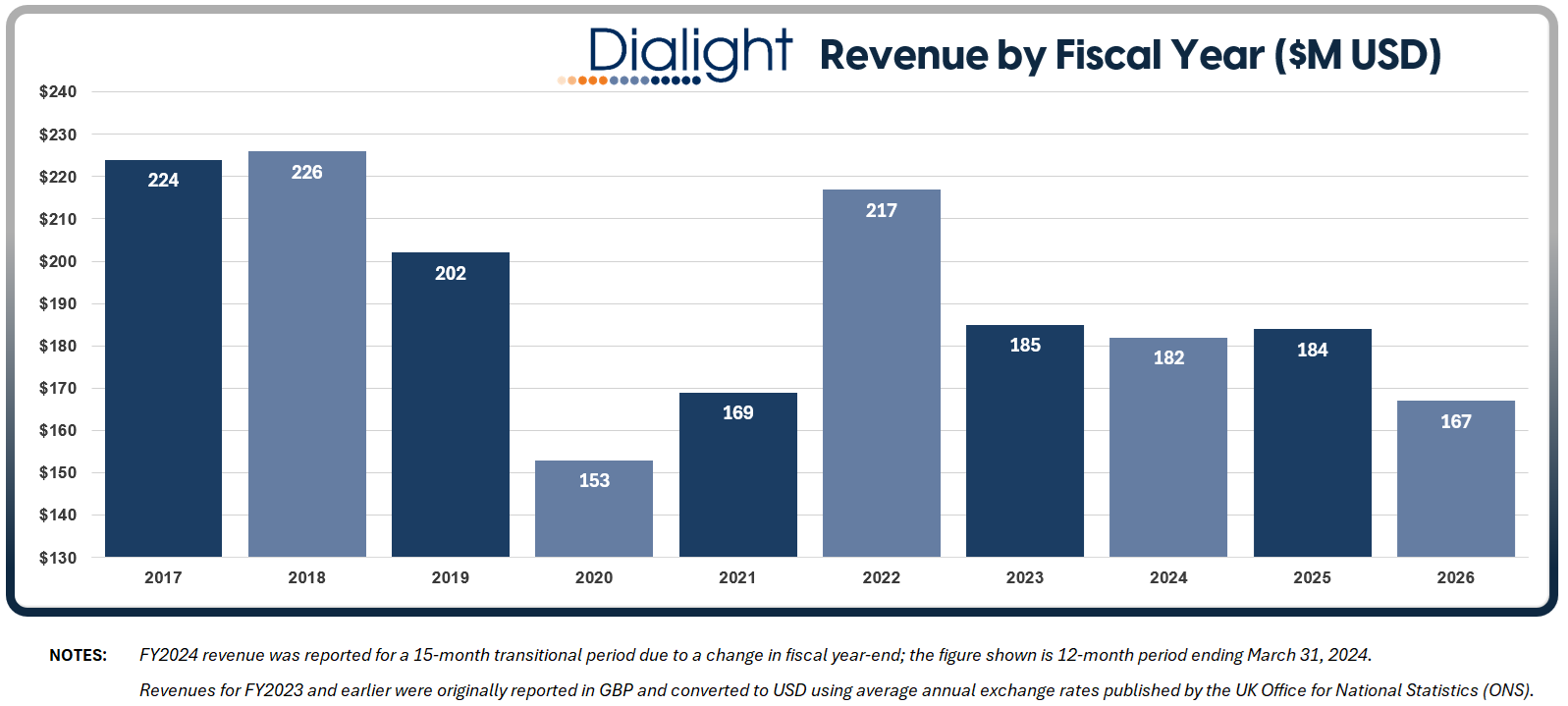

Revenue fell 9% to $166.9 million, making FY2026 the company's second-lowest annual total in over a decade, trailing only the pandemic-impacted FY2020. The trend line is not flattering.

From a 2015 peak, Dialight has given back roughly $70 million in annual sales over a period defined by executive turnover, litigation, and a fundamental rethinking of how the company operates. North America, which generates approximately $139.9 million of that revenue, remains both the engine and the exposure.

And yet, the FY2026 report may be the most encouraging Dialight has produced in years.

The Numbers That Tell the Better Story

Underneath the revenue decline, nearly every other metric moved sharply in the right direction. Underlying operating profit more than doubled, from $4.2 million to $10.3 million. Gross margin expanded 340 basis points to 39.0%. Operating cash flow climbed to $34.2 million from $19.7 million. Net bank debt fell from $17.8 million to $1.9 million, a level that was nearly unthinkable eighteen months ago.

Inventory dropped 36% to $30.0 million in a single year. For lighting people who understand what inventory levels signal about a manufacturer's operational health, that number carries as much weight as any profit figure. The Sanmina litigation, which cost the company more than $17 million in charges during FY2025 alone, is now fully resolved after a $5.7 million final payment in December 2025.

The Lighting Segment Carries the Drag

Dialight's core lighting business, roughly 75% of group revenue, saw sales decline 11.5% to $122.1 million. Management attributes the weakness to deferred industrial capital projects, tariff uncertainty, and geopolitical disruption. Those explanations are credible. Oil and gas, heavy manufacturing, and large infrastructure projects form the backbone of Dialight's specification pipeline, and capital project deferrals are a documented reality across those sectors.

What the report does not address directly is market share. The company's risk disclosures acknowledge competitor reduction in force as a marker of broader market contraction, but Dialight does not provide enough granularity to separate market-driven revenue loss from share-driven loss. That distinction matters considerably for anyone assessing whether FY2027 growth will be a tide coming back in, or a harder climb.

The more promising signal came late in the year. Fourth-quarter order momentum strengthened, and the backlog entering FY2027 has grown more than 25% versus the prior year-end. Whether that backlog converts to shipped revenue at the expected pace is the central question management now has to answer.

Signals & Components: The Quiet Rebound

While lighting contracted, Signals & Components delivered a result worth noting. Excluding the exited Traffic business, segment revenue grew 13.7%, and underlying operating profit reached $8.4 million against $3.3 million the prior year. Gross margins expanded nearly 960 basis points to 34.2%.

Management has repositioned this segment around opto-electronic components used in data centers and AI-related equipment, areas where Dialight's products sit inside servers and industrial gear. The AI connection is not a transformation narrative yet, but it is one of the few places inside the company where the growth arrow is pointing the right direction and investment is following.

The USMCA Advantage, and What It Requires

Dialight's primary manufacturing in Ensenada, Mexico currently operates largely tariff-free under the USMCA agreement. Tariff impacts on material costs were less than 1% for the year. That protection has provided a margin buffer that competitors manufacturing elsewhere have not fully enjoyed.

The company is now transferring its Roxboro, North Carolina operations to Mexico, which will further concentrate production there. Dialight's own risk disclosures flag cartel-related security concerns and rising Mexican regulatory pressure as live operational risks. The USMCA advantage is real. So is the concentration cost if conditions shift.

Dialight enters FY2027 with its cleanest balance sheet in years and a transformation plan that delivered on its operational promises. Revenue growth is the next proof point, and unlike cost restructuring, it cannot be achieved through internal discipline alone.