March 12, 2026

Earnings Calls: The Lighting Industry's Weather Report

Guest author: Geoff Marlow

The market isn’t collapsing, but it’s cooling, and the public companies have already adjusted.

If you run a privately held lighting manufacturer or an independent rep agency, you probably don’t spend much time reading public-company earnings transcripts. That’s understandable. Most of those calls are aimed at portfolio managers and analysts, not operators deciding whether to approve a new product line or hire another spec writer.

But you should be paying attention.

Not because Signify’s stock price affects your backlog — it doesn’t. But because the language coming out of these companies acts as a barometer for the broader market. When the largest players start talking about cost restructuring, pricing pressure, and disciplined capital allocation, they’re describing atmospheric conditions that eventually reach everyone.

Think of it as a weather system. The public companies are the early-warning stations. They have institutional sensor networks — investor analysts, global supply chains, quarterly reporting cycles — that detect shifts before most private operators feel them in the order book.

Right now, the barometer is falling. Not crashing. Falling. The question for every mid-market manufacturer and regional rep agency is whether your operating posture reflects current conditions — or last year’s forecast.

What the Public Companies Are Signaling

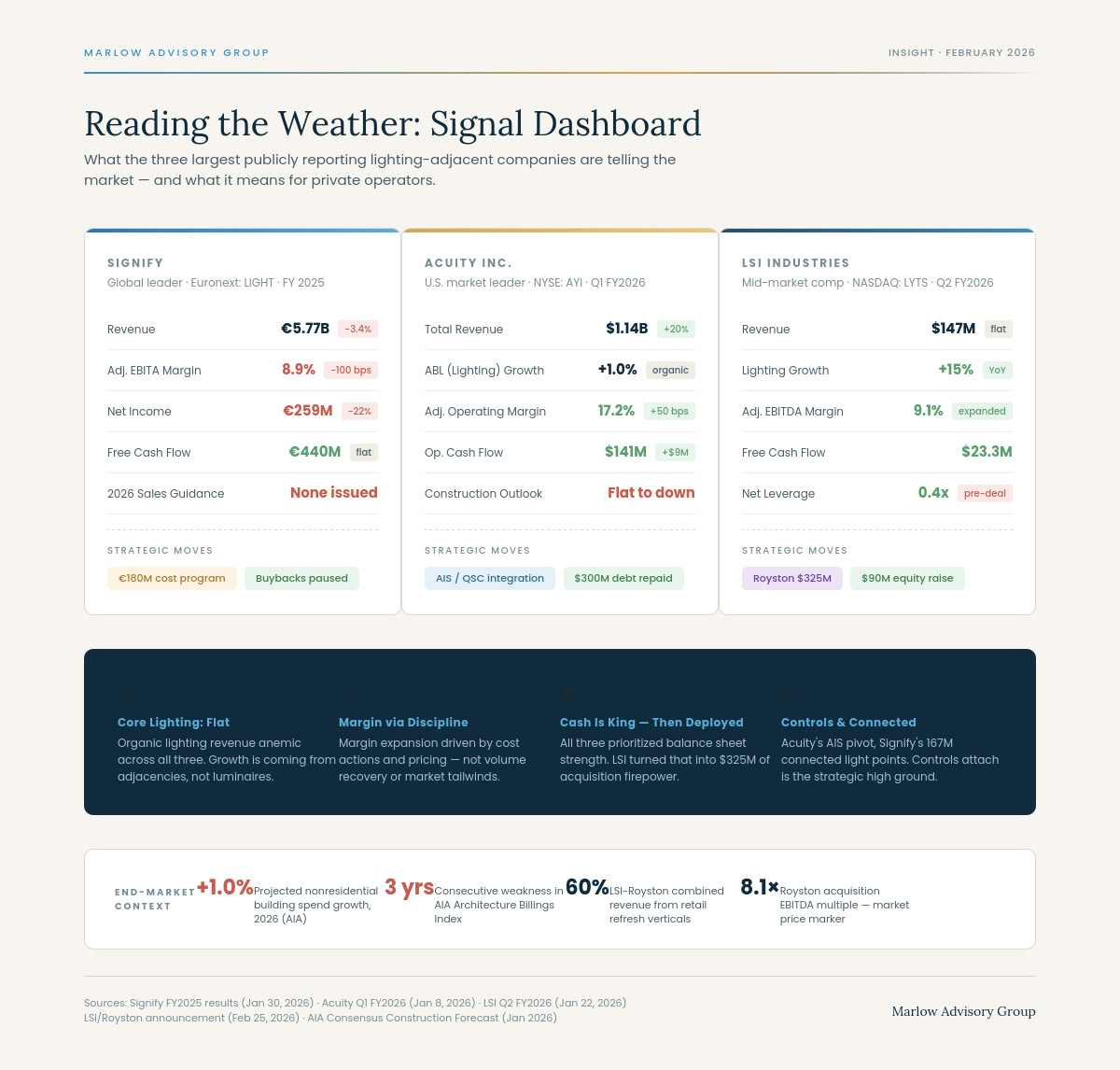

Three companies offer a useful cross-section of the market: Signify, Acuity, and LSI Industries. They span global and domestic, architectural and commercial, specification and value-engineered. Their recent results paint a consistent picture.

Signify (full-year 2025 results) reported full-year 2025 sales of €5.77 billion — a comparable decline of 3.4%. Adjusted EBITA margin compressed from 9.9% to 8.9%. Net income dropped to €259 million from €334 million. The response: a €180 million cost reduction program, a pause on share buybacks, and a decision not to issue full-year 2026 guidance.

That last point deserves emphasis. When a company with market intelligence across more than seventy countries declines to provide a revenue outlook, they’re not being coy. They’re telling you they don’t have enough visibility to commit. Price pressure in trade channels intensified throughout the year. The professional market in Europe remains weak. The U.S. showed pockets of strength — not enough to offset the drag.

Acuity (Q1 FY2026 results) told a different story, but with shared undertones. Fiscal Q1 2026 looked strong on the surface: $1.1 billion in net sales, 20% year-over-year growth, adjusted operating margins expanding to 17.2%. Strip away the QSC acquisition, and the core lighting business grew just 1%. Management was explicit: they don’t expect a recovery in commercial construction or retrofit demand. The margin story was about cost discipline and restructuring — not volume growth. Meanwhile, they’re allocating capital toward controls, technology, and connected systems. That’s an unmistakable signal about where future value creation lives.

LSI Industries (Q2 FY2026 results), more directly comparable to many mid-market operators, held revenue flat at $147 million in their fiscal Q2 2026. Their lighting segment posted 15% growth and meaningful margin expansion, but display solutions declined 10%. The narrative: price optimization, productivity improvements, and disciplined working capital management. They reduced total debt by $22.7 million during the quarter and generated $23.3 million in free cash flow. It looked like a company in fortress mode — protecting the balance sheet, building optionality.

Then, on February 25th, LSI revealed why.

The company announced a definitive agreement to acquire Royston Group — an Atlanta-based, vertically integrated provider of custom store fixtures, retail signage, and refrigerated display cases — for $325 million. Royston brings approximately $272 million in trailing revenue at a 14% adjusted EBITDA margin, materially above LSI’s own 9.7%. The combined entity will generate roughly $864 million in pro-forma revenue and $95 million in adjusted EBITDA. Royston’s revenues are concentrated in refueling, grocery, and convenience store markets — verticals driven by retail refresh cycles and brand identity programs, not construction starts.

This is the most important signal in the deal: LSI didn’t deploy $325 million into construction-dependent segments. They went deeper into retail branding, where demand runs on its own cadence. The balance sheet discipline wasn’t just defense. It was ammunition. They cleared leverage to 0.4x precisely so they could move aggressively when the right asset appeared.

For any mid-market operator reading this, the lesson is pointed: cash discipline creates optionality. Without it, you’re not a buyer. You’re inventory.

The synthesis across all three companies: revenue growth in core lighting is anemic at best. Margin protection is coming from cost management and pricing discipline — not market tailwinds. Cash and balance sheet strength are clear priorities. Controls and connected systems are the strategic focus. And nobody is counting on the construction cycle to bail them out — LSI’s Royston deal makes that explicit.

The AIA Consensus Construction Forecast published in January 2026 reinforces the point. Nonresidential building spending likely declined modestly in 2025 and is projected to grow just 1% in 2026 — not keeping pace with inflation. The Architecture Billings Index has been in negative territory for over three years. Outside of data centers, commercial construction is soft across most categories. These are the end-market conditions your products ship into.

If You Run a $30–$75M Lighting Manufacturer

The public companies are doing their homework. The question is whether you’re doing yours.

Inventory and Product Mix

If you haven’t done a rigorous SKU rationalization in the last twelve months, you’re carrying dead weight. The post-COVID supply chain scramble incentivized breadth — stock everything, promise everything, ship anything. That logic is now working against you. Every slow-moving SKU ties up cash, consumes warehouse space, and complicates your manufacturing schedule.

Pull the data. Identify the bottom 15–20% of your catalog by velocity and margin contribution. Have the hard conversation about what gets pruned.

Then look honestly at your controls attach rate. Acuity is investing aggressively in intelligent spaces. Signify continues to lean into connected lighting as a strategic differentiator. If your luminaires ship without a controls story — or if your spec team can’t confidently walk a customer through an nLight or Lutron alternative — you’re ceding the highest-margin portion of the project to someone else. Controls competency isn’t optional anymore. It’s table stakes for specification work, and specification work is the only sustainable competitive position for a mid-market manufacturer.

Pricing Discipline

This is where private companies routinely lose the plot in soft markets. The instinct is to chase volume — flex on pricing to keep the plant running. I understand the logic. But the public companies are showing you a different playbook: protect margin, even at the expense of top-line growth. When LSI talks about “price optimization” delivering margin improvement on flat revenue, that’s not an accident. That’s a deliberate choice.

Audit your discount governance. Who has pricing authority, and what are the guardrails? If every regional manager can cut price by 8–10% without escalation, you don’t have pricing discipline — you have a suggestion.

Establish clear rules: where you’ll hold the line (specification-grade products, controls-attached projects, differentiated applications) and where you’ll flex (commodity replacements, highly competitive bid-and-ship work where you have genuine cost advantage). The goal isn’t rigidity. It’s intentionality.

Cash and Balance Sheet

Every company I cited is managing cash with visible urgency. Signify paused buybacks. Acuity voluntarily repaid $300 million in debt across fiscal 2025 and the start of fiscal 2026. And LSI’s story is the most instructive: they spent quarters methodically driving leverage to 0.4x — then deployed $325 million to acquire Royston at a moment when they had the balance sheet strength to act on their own terms. They didn’t need permission. They had optionality because they’d earned it.

For a $40M–$75M private manufacturer, the message is clear. Tighten your AR collection cycle. Review your payment terms — are you financing your customers’ working capital at your expense? Scrutinize every capital expenditure over $100K. If you’re carrying variable-rate debt, model the impact of rates staying elevated through 2026. The AIA and Dodge forecasts don’t project a meaningful uptick in nonresidential activity until late 2026 or 2027. Your balance sheet needs to be built for a longer flat stretch — not a quick recovery.

If You Run a Regional Rep Agency

For rep agency owners, the signals carry a different set of implications — but the urgency is the same.

Start with your line card. When Signify announces a €180 million restructuring and declines to give revenue guidance, that ripples down to every agency carrying their lines. When LSI announces a $325 million acquisition redirecting significant revenue toward retail branding verticals, every agency carrying LSI lighting lines should be asking what that means for product emphasis going forward. Not necessarily as an immediate problem — but as a risk factor you need to understand.

Are your principals financially stable? Are they investing in controls, connected systems, and specification-grade products where the growth is? Or are they riding a legacy catalog into a softening market? These are questions you should be asking out loud, not hoping someone else answers.

Underwriting Your Line Card

Think about your line card the way an investor thinks about a portfolio. Each principal represents a position. You’re investing your sales force’s time, your spec team’s relationships, and your agency’s reputation. What’s your concentration risk? If 40% of your commission revenue comes from one manufacturer in a commodity segment facing margin compression, you have a single-point-of-failure problem that no amount of relationship history will protect you from.

Evaluate each principal on financial health, product trajectory, controls capability, specification relevance, and market positioning. Assign an honest grade. Then have the uncomfortable conversation about whether your line card is positioned for where the market is heading — or where it was three years ago.

Beyond the line card, invest in your own competency stack. The agencies that thrive here will have deep controls knowledge, strong specification relationships, and the ability to provide genuine project-level technical support. If your value proposition is logistics coordination and lunch-and-learns, you’re vulnerable. If you can walk an engineer through a controls integration and defend a specification against value-engineering pressure, you’re essential. The market is about to clarify which one you are.

The Gap Between Public Discipline and Private Comfort

Public companies move faster — not because they’re smarter, but because the market forces them to. Quarterly reporting, analyst scrutiny, and share price accountability create a compressed decision cycle. When Signify sees demand softening, they announce a €180 million restructuring the same quarter. When Acuity sees flat lighting revenue, they reallocate capital immediately. When LSI sees an opportunity, they clear leverage and write a $325 million check.

Private operators have more latitude. And that latitude can become a liability.

Without the external pressure of public markets, it’s easier to defer difficult decisions. Easier to carry the underperforming SKUs another quarter. Easier to keep the discount structure loose because the sales team is pushing back. Easier to delay the product portfolio conversation.

There is a cost to waiting. Every quarter you defer SKU rationalization, you’re burning cash on inventory that won’t sell. Every month you tolerate undisciplined pricing, you’re eroding the margins you’ll need when volumes compress further. Every year you delay investing in controls competency, you fall further behind competitors who started years ago.

The public companies are telling you, in plain language, what they see. The conditions they describe — price pressure, demand softness, backlog normalization, construction cycle uncertainty — aren’t unique to companies with $1 billion in revenue. They’re market conditions. Your market.

The weather has shifted. The public companies recalibrated months ago. They’ve restructured costs, tightened capital allocation, and redirected investment toward durable demand. One of them just bet $325 million that the future isn’t in waiting for the construction cycle to turn.

The question for every privately held manufacturer and rep agency in this industry is straightforward: is your operating posture aligned with the conditions you’re actually in — or the conditions you’re hoping will return?

Hope is not a strategy. It never has been. And the barometer doesn’t care whether you’re reading it.

Geoffrey Marlow

Geoff Marlow brings over 30 years of unparalleled experience and achievement to the industry, solidifying his reputation as a principled leader and innovative strategist. He has held senior-most executive roles across mid-sized specialty manufacturers, multi-billion-dollar manufacturing enterprises, and as an entrepreneurial start-up manufacturer's representative within a top 10 construction market. Most notably, Geoff led his start-up representative agency to unprecedented success, growing it into the largest agency in its market within just five years.